Late-cycle goldilocks scenario

- Jarosław Jamka

- 10 sty 2024

- 1 minut(y) czytania

Subjective market review (10-Jan-2023), or what recently caught my attention in several points:

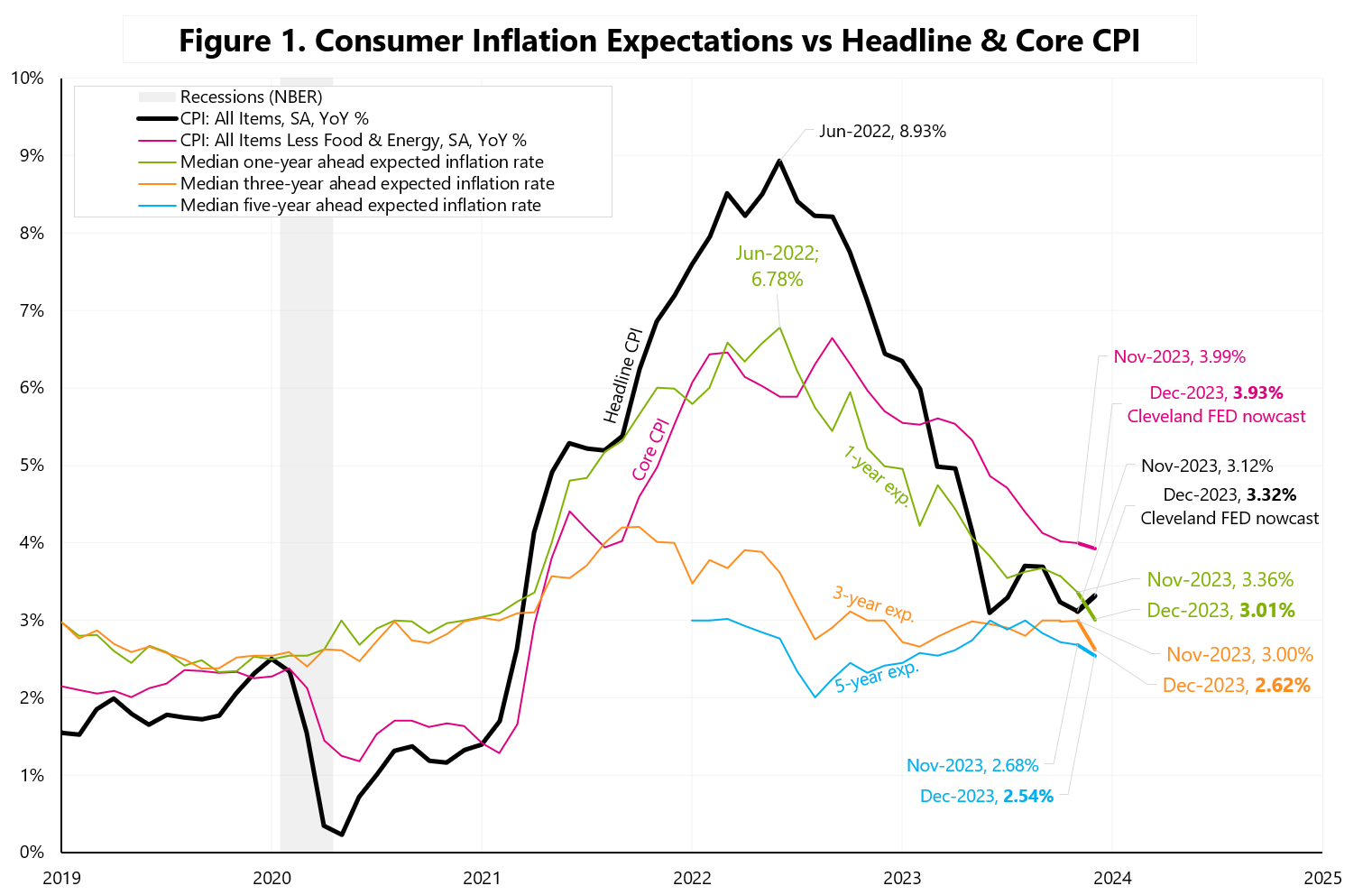

1) A week with inflation, i.e. quite a good/soft series of various data on inflation - so far, still waiting for China (today) and the USA inflation data (tomorrow and Friday):

(i) a strong decline in inflation expectations in the New York Fed's latest Survey of Consumer Expectations (decline in inflation expectations at all time horizons).

(ii) Lower inflation in Japan for December on a headline basis (+2.4% vs. +2.7% in Nov and vs. the Street's +2.5% forecast),

(iii) further decline in used car prices (but only a 2.52% share in the CPI basket, compared to New Vehicles with a share of 4.23%): The Manheim Used Vehicle Value Index fell 0.5% in December.

2) Oil also supports inflation...price declines this week after Aramco reduced its OSP (official selling price) in oil supplies to its main customers next month - which is usually interpreted as a sign of weaker physical demand. The growth is not surprising strongly upwards (like > 4% in Q3 2023): currently Atlanta Q42023 GDP tracker only +2.2% (the employment situation, ISM services and auto sales saw the Atlanta Fed fall from 2.5% to 2.0%; however, yesterday after the trade data it was revised up to 2.2%).

3) As a result, we have a kind of "late-cycle goldilocks scenario": growth is slowing down, but not too much, inflation will not be a problem in the short term, and we are starting interest rate cuts as in 2019. This supports the technology sector and Mag7, but on a relative basis not supports strongly cyclical countries/markets (e.g. Poland). In 2019 S&P500 +28.9%, WIG30 -4.2%.

Komentarze